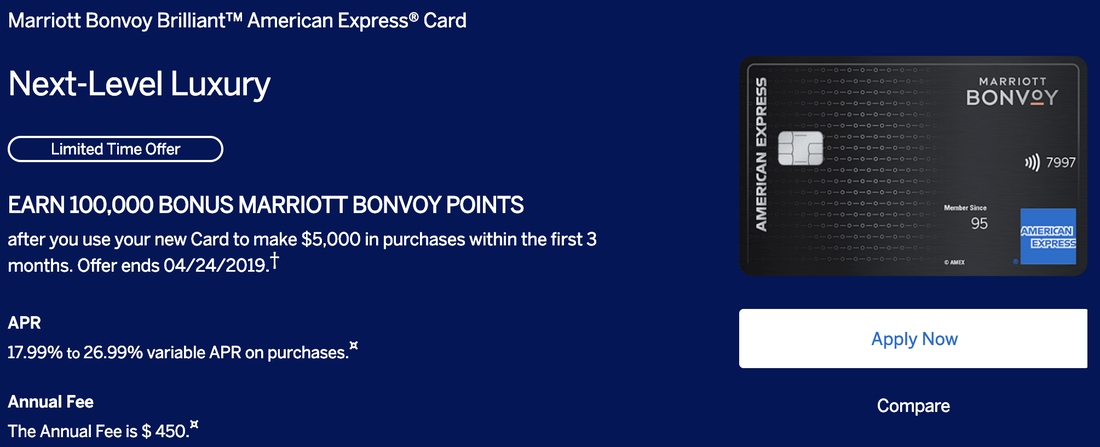

With the new name for the world's largest loyalty program unveiled, the Starwood Preferred Guest American Express Luxury Card is finally rebranded as the Marriott Bonvoy Brilliant American Express Card. Everything remains the same but the name - including (1) the $450 annual fee, (2) 100,000 Marriott Bonvoy bonus points after you spend $5,000 within the first 3 months of new account opening, (3) annual $300 credits at any Marriott portfolio hotels worldwide, (4) an annual free night at Marriott portfolio hotels or resorts with a redemption level of 50,000 points or less, (5) annual 15 night credits towards Marriott elite status, (6) free Marriott Gold status and upgrade to Marriott Platinum status after $75K annual spending, and (7) Priority Pass Select membership with unlimited airport lounge access for you plus two guests.

At the same time, the Starwood Preferred Guest Business Card from American Express is rebranded as the Marriott Bonvoy Business American Express Card. The only thing that changes other than the name is the annual fee - increased from $95 to $125 and NOT waived for the first year any more. However, if you apply before 3/28/19, you will continue to receive the first annual fee waiver and your annual fee after the first year will be grandfathered in at $95. You will also receive 100,000 Marriott Bonvoy points after spending $5,000 within the first 3 months. If you have been thinking about applying for this card, you probably want to do it before March 28.

At the same time, the Starwood Preferred Guest Business Card from American Express is rebranded as the Marriott Bonvoy Business American Express Card. The only thing that changes other than the name is the annual fee - increased from $95 to $125 and NOT waived for the first year any more. However, if you apply before 3/28/19, you will continue to receive the first annual fee waiver and your annual fee after the first year will be grandfathered in at $95. You will also receive 100,000 Marriott Bonvoy points after spending $5,000 within the first 3 months. If you have been thinking about applying for this card, you probably want to do it before March 28.

RSS Feed

RSS Feed