August 26, 2018 is a date when several Chase credit card related changes kick in. First of all, Chase has eliminated two consumer protection benefits: Price Protection (for all Chase cards) and Return Protection (for Sapphire Preferred, Freedom, Freedom Unlimited, Ink Preferred, United Explorer, and probably other products). Secondly, Korean Air which used to be a great transfer partner for redeeming Ultimate Rewards points has been removed; on the other hand, JetBlue is added as a transfer partner and the transfer ratio of 1:1 is actually better than the competitors' (Amex Membership Rewards, Citi ThankYou, Marriott Rewards). Lastly, JPM Ritz-Carlton Visa Infinite, which has been discontinued to new applications since late last month, receives two enhancements for its existing cardmembers - an annual Marriott portfolio free night capped at 50K points and one extra point earning for all categories. If you currently have this card, there are many reasons to keep it as long as you can.

In addition, we regularly review the current and recent (within a year) signup bonuses as well as the availability of the top credit cards for adjustment of our ranking. As a result, our Top 10 Best Credit Cards list has been updated. Below is a before and after comparison.

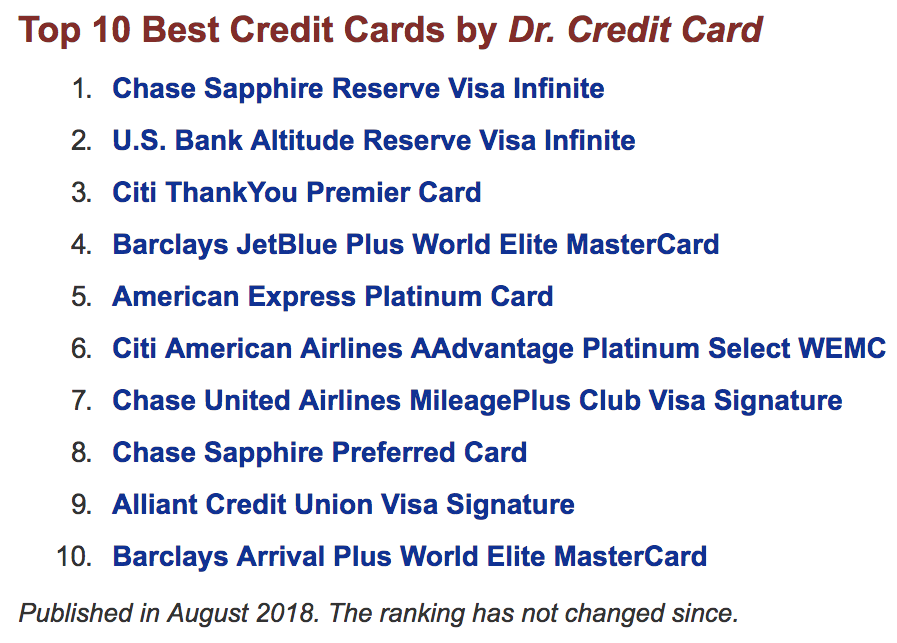

In addition, we regularly review the current and recent (within a year) signup bonuses as well as the availability of the top credit cards for adjustment of our ranking. As a result, our Top 10 Best Credit Cards list has been updated. Below is a before and after comparison.

As you can see, Amex SPG Card, which used to be a powerhouse for general spending, has disappeared from the list because the earning rate has been reduced from 3x Marriott points (i.e. 1x SPG points in the old system) to 2x Marriott points as of August 1, 2018. Citi Prestige, which has been pulled from Citi website and unavailable to new applications but will be relaunched in the near future, has been removed as well (hopefully temporarily). Chase United Club Visa is now #7 due to the consistent signup bonus of 50K miles. Also note that the enhanced JPM Ritz-Carlton Visa could have landed on this prestigious list for the very first time and also replaced Amex Platinum Card as the #1 Credit Card for Perks if it has not been discontinued to new applications, and unlike Citi Prestige, it seems that Chase has no plan of relaunching this premium card due to the Marriott-Amex-Chase agreement that makes Amex the issuer of premium Marriott credit card.

RSS Feed

RSS Feed