This week we have seen some elevated signup bonuses on a few credit cards (our value for the bonus minus first year annual fee is for your reference - your valuation may vary):

- Amex Gold Delta SkyMiles personal card ($95 annual fee, waived for the first year): 60,000 miles + 5,000 MQMs (Medallion Qualifying Mile) - our value $650

- Amex Gold Delta SkyMiles business card ($95 annual fee, waived for the first year): 70,000 miles + 5,000 MQMs - our value $750

- Amex Platinum Delta SkyMiles personal card ($195 annual fee): 75,000 miles + 5,000 MQMs + $100 statement credit - our value $705 (historical high)

- Amex Platinum Delta SkyMiles business card ($195 annual fee): 80,000 miles + 5,000 MQMs + $100 statement credit - our value $755 (historical high)

- Amex Delta Reserve personal card ($450 annual fee): 75,000 miles + 5,000 MQMs - our value $350 (historical high)

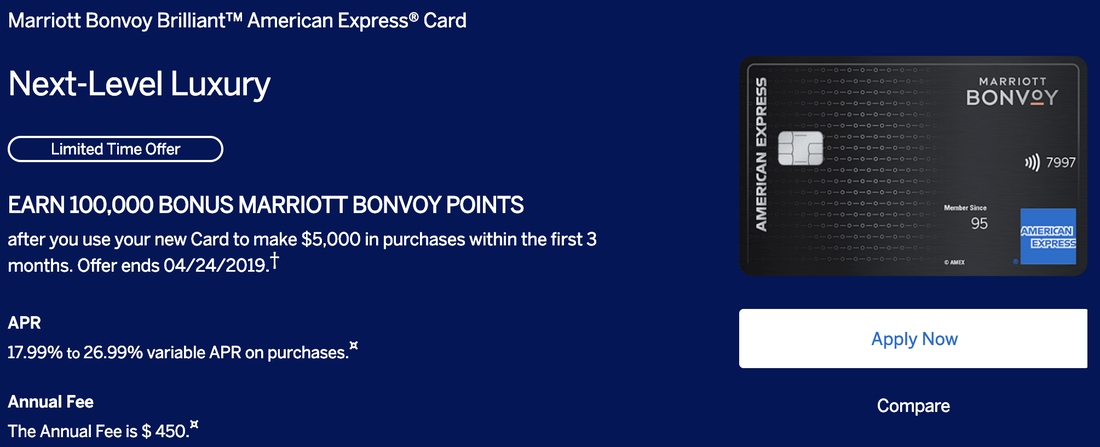

- Chase Marriott Bonvoy Boundless Visa ($95 annual fee): 100,000 points - our value $655 (historical high)

- Chase IHG Rewards Club Premier MasterCard ($89 annual fee): 120,000 points - our value ($390 (historical high)

RSS Feed

RSS Feed